Investment strategies and outlook

DESPITE a slowing in global growth, investment markets proved resilient in 2019.

Global equities, including the Australian market, have returned close to 20 per cent in AUD terms, led by the Nasdaq which has risen more than 25 per cent.

Australian bonds are approaching double digit returns.

The year finishes much different to how it started.

The US Federal Reserve (the Fed) has turned from raising rates to cutting rates.

The RBA changed from saying the next move is up in rates to also cutting rates, and openly discussing the possibility of quantitative easing (QE).

Bonds have rallied significantly as yields have fallen. Equity markets have set new highs with developed markets outperforming emerging markets.

The technology sector has been a standout and the USD has been strong.

2020 Predictions

For Australia, our outlook remains optimistic and we expect GDP growth to pick up to 2.8 per cent supported by infrastructure investment.

We note the recent policy announcement by Treasurer Frydenberg to provide tax breaks for foreign capital starting large infrastructure projects.

More monetary easing is to come from the RBA, but what form it takes is uncertain at this stage.

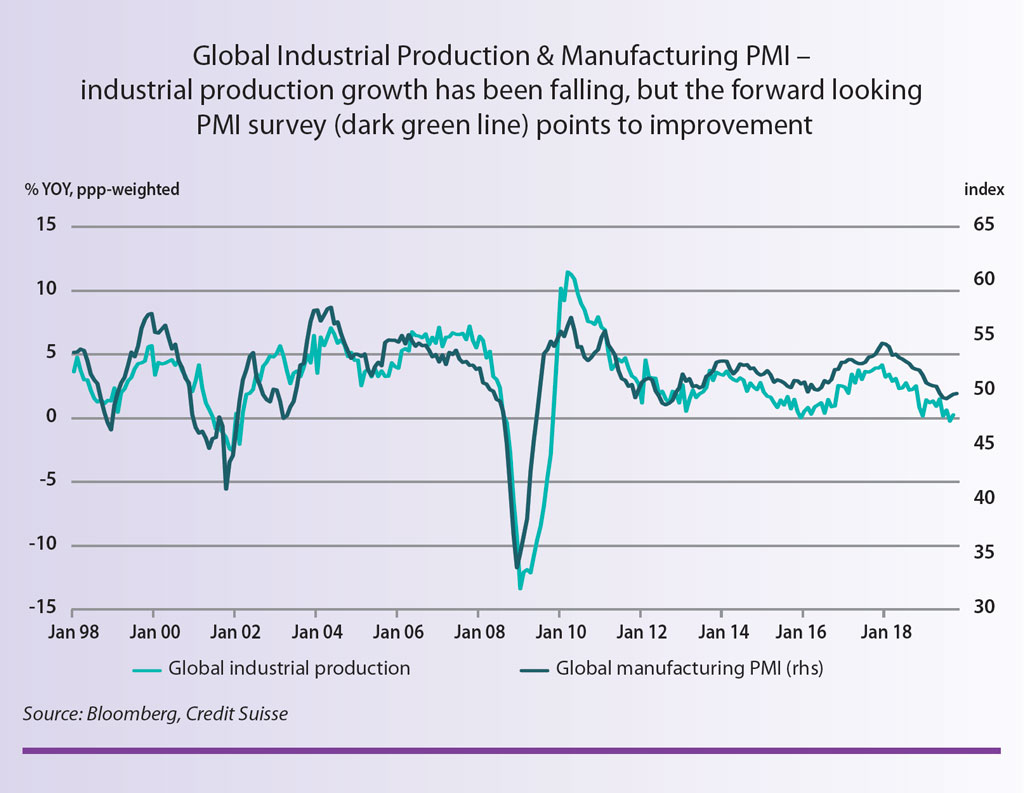

Credit Suisse believes global growth will be a sluggish 2.5 per cent in 2020 with a mild recovery in industrial production.

De-escalation of the trade war should reignite capital spending in the US and China, and Brexit should finally be put to bed.

There is sentiment risk attached to the US election, particularly as the leading Democrat contender has strong views on regulating Wall Street and the break-up of big tech.

Inflation is under control, but may rise temporarily in the US.

The Fed is unlikely to cut rates again and the US should produce GDP growth of 1.8 per cent.

European growth is likely to be stalled at 1 per cent, although resolution of the trade dispute will help exports.

Chinese growth will be a little lower in 2020 compared with 2019 at 5.9 per cent, but still outstrips most of the rest of the world and will benefit from moderate stimulus.

Returns on most core international government bonds are likely to be negative, except for the USA, which is benefiting from higher yields.

Australian government bond yields are likely to range trade as the local economy searches for impetus, but should eke out a small positive return.

On the other hand, it is difficult to see a positive return for Swiss and European bonds. Within the bond asset class we have a preference for certain corporate investment grade bonds in developed markets, subordinated credits in the financial sector such as those issued by the Australian banks, and high quality covered bonds.

Limited earnings growth should translate into single digit returns for the global share market.

As we expect a mild recovery in growth, we enter 2020 overweight in emerging markets and also prefer financials as a sector, given leverage to a likely steeper yield curve.

The key risks are lingering trade uncertainty surrounding the tariff negotiations, and upheaval in the Middle East and Hong Kong.

The major economic risk is probably higher than expected inflation, particularly in the US, which would lead to tighter monetary policy.

We favour equities over bonds, and in developed markets have a preference for US equities given superior growth prospects and a large technology sector that will benefit from better economic activity.

Technology is also benefiting from long-term trends in digitisation, automation and artificial intelligence.

With cash our least favoured asset class and lower returns expected for equities and bonds, alternatives look attractive given lower for longer rates and yields.

Hedge funds are a broad church but should provide single digit returns uncorrelated with any particular liquid market and improve portfolio stability.

Direct real estate exposure in industrial property and flexible office space should continue to benefit from long-term trends in digital retail and business disruption.

Accessing such opportunities is difficult but fund options are available to diversify the risk. Finally, private equity (PE) provides an alternative source of return.

We are concerned about some examples of PE managers selling assets to other PE managers and so pushing values and returns up, without being tested by for example the IPO or other open market.

To avoid future issues around this we like seasoned managers who are top quartile performers.

Our research shows the best performers in PE exhibit persistence in returns.

Also, we have biased our PE exposure to medium sized managers who are more nimble and operate in the part of the PE market with easier competition for assets.

Overall, we enter 2020 optimistic, like we did in 2019.

Returns will be lower than 2019, but nonetheless we see 2020 building on what has been a stellar year.

Andrew McAuley is Credit Suisse chief investment officer. The information provided is the opinion of the author. The AJN recommends that readers seek independent financial advice.

comments