Survival in a volatile world: here’s what some leading investors are doing

Normally when markets are at their lows central banks can cut interest rates and stimulate economies. “There’s no put option from central banks,” Dr Kasian says, referring to the famous “Greenspan put” used by former US Federal Reserve chairman Alan Greenspan to pump up the economy when trouble struck.

ROD MYER

The last 10 months have been a volatile time in the financial markets. Just when investors were starting to get real confidence back as the trauma of the global financial crisis disappeared from their rear vision mirrors, panic broke out again.

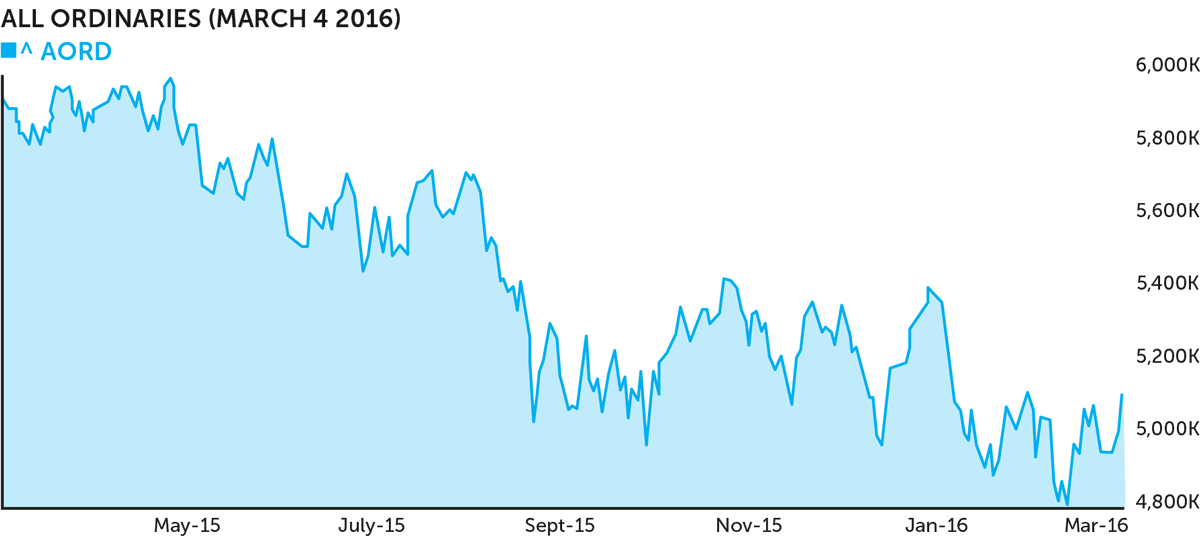

In Australia the S&P ASX 200 index peaked at 5996.9 in April 2015 then turned down. Big slides in August and October were followed by a rebound towards year’s end. Then a death defying plunge from the beginning of 2016 which has seen it move into bear territory at lows of 4706.7.

Overseas the picture is mixed. European markets are generally in bear territory but the US is holding its end up with the market only down 11 per cent. Spare a thought for Chinese investors however with the Shanghai Composite index down as much as 53 per cent.

A bear market is one which falls 20 per cent. It begins when confidence is high and catches many people unaware.

We’ve seen this before

For students of history the current conditions should not surprise. “We’ve had 14 bear markets in the last 40 years,” says Paul Kasian, head of asset management with Equity Trustees, (EQT) a group with $5 billion under management.

“You’ve got to prepare clients for that all the time as there’s a tendency with human nature to panic.”

Dr Kasian advises against panic as an unproductive and risky state of mind when it comes to investment and points to history as a guide. “The market’s no more excessively volatile than it has been a number of times in the past.”

“It’s not like the Global Financial Crisis (GFC) and its not the crash of 1987 either,” Dr Kasian says.

The famously phlegmatic Reserve Bank of Australia governor Glenn Stevens has also called for calm saying fears are “overdone” and observed financial markets are “almost pricing as though there will be a global recession. I think that might be a bit pessimistic really … but, you know, it remains to be seen,” he said.

Students of the market say keeping a weather eye to market conditions while ensuring you have a resilient and well structured portfolio is the key to survival.

Rene Pyszko, head of investments at Commonwealth Private Office, has helped prepare clients for the current situation. “Around June or July last year we foresaw increased volatility because of the potential for a rise in US interest rates for the first time in a decade.”

“We didn’t foresee the degree of the volatility. But we did reposition a lot of our clients over the past six months” Pyszko says.

Repositioning in volatility

The repositioning looks like this. In constructing a portfolio Pyszko starts from a position of 50 per cent defensive assets which might include various types of fixed interest and some types of property. The other 50 per cent is in growth assets like equities.

While growth assets are only 50 per cent of the starting point portfolio, they represent 80 per cent of the actual risk carried. That starting point portfolio is too conservative for most of Pyszko’s clients who generally have 60 per cent in growth assets.

Mid last year Commonwealth “introduced a more defensive fixed income manager to the portfolio that would add value if volatility increases.”

The next move was to “reduce our allocation to emerging markets” which he favours in the long term because of their favourable demographics and growth prospects. However the end of the resources boom has seen markets like Brazil collapse and Russia experience wild swings and China, as observed earlier, has lost over 50 per cent of its market value as its mighty economy slows.

Another factor weighing on emerging markets is the recent US rate rise and stronger dollar which make life difficult for .emerging economies to pay off their US dollar debt.

This is new

Before working out what to do from here it’s worthwhile teasing out what some of the current risks might be. EQT’s Paul Kasian says there is one difference between now and previous bear markets; the world’s central banks have lost their fire power.

Normally when markets are at their lows central banks can cut interest rates and stimulate economies. “There’s no put option from central banks,” Dr Kasian says, referring to the famous “Greenspan put” used by former Federal Reserve chairman Alan Greenspan to pump up the economy when trouble struck.The value in such investment has been two fold. Not only have some markets, like the US, fallen less than Australia’s in recent times, the currency effect has been a powerful driver of profit.

The value in such investment has been two fold. Not only have some markets, like the US, fallen less than Australia’s in recent times, the currency effect has been a powerful driver of profit.

That option no longer exists because in many countries interest rates are almost zero. In fact in Sweden and Japan central banks have instigated negative interest rates in an attempt to force people to take money out of the banks in invest it in economic activity. Negative rates mean the bank charges you a fee to look after your cash for you.

The risk here is deflation, Dr Kasian says. “Inflation’s a wonderful thing when everyone’s got a lot of debt (as the size of your debt in real terms is reduced). But now everyone’s got a lot of debt and they’re worried about deflation,” he says.

Deflation is a double whammy, Not only does debt grow in a relative sense but with prices falling consumers put off purchases as they will be cheaper tomorrow and that clobbers growth further.

But it’s unlikely to happen. “The central banks will print money like there’s no tomorrow to prevent deflation. I believe it’s a very low probability,” Dr Kasian says.

While there is still plenty of risk there could be opportunities emerging. Pyszko says some of his ultra- high new worth clients are seeing opportunity. “Some clients who might have been balanced have used market volatility to actually add to positions and we’ve made some initial increases to portfolios.”

“Others have been more conservative and worry about capital preservation.

On the property side some Commonwealth clients are cooling towards residential property because the market has run so strongly and others are balancing portfolios away from mid-sized commercial property in suburbia that can be hard to rent.

Property, Pyszko says, should be looked at on a case by case basis, Commercial property needs to have “a great tenant and prime location,” he says.

Some of his clients have even ventured into the US property market taking advantage of the weakness after the GFC or looking for quality assets, especially when the Australian dollar was high. “It’s not something we have expertise in but we certainly help them facilitate it, of the bank helps through the lending side of things,” Pyszko says.

There have been some important lessons learnt by investors in recent years. “We’ve been educating our clients about buying international equities and listed property. And global fixed interest has been a rich opportunity.”

The value in such investment has been two fold. Not only have some markets, like the US, fallen less than Australia’s in recent times, the currency effect has been a powerful driver of profit.

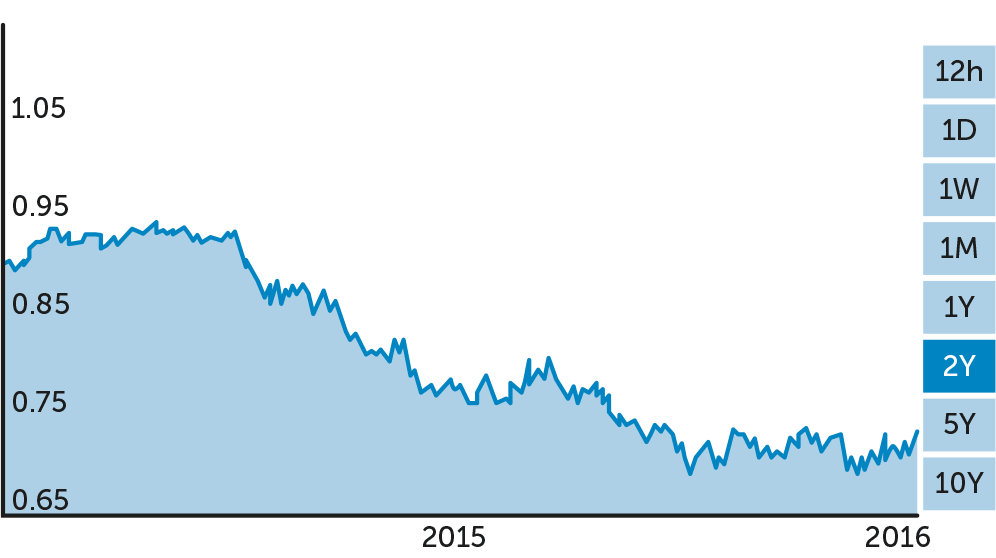

Since 2013, the Australian dollar has fallen from parity with the Greenback to currently around US71c. That means US dollar denominated assets are worth 29 per cent more in local currency than they were when there was parity.

Paul Kasian says EQT tends towards a passive approach to investing internationally. That means choosing funds that hug the index in their chosen market rather than fund managers who pick particular stocks they see as having extra potential.

When required EQT will choose an active manager in fixed interest or equities The approach taken “will depend on the needs and risk profile of the client”. Dr Kasian says.

Very occasionally EQT will choose an active manager in fixed interest or equities if “there’s a very good argument for it,” Dr Kasian says.

Don’t ignore fixed interest

The other asset class Australians traditionally shun is fixed interest and this has been to their detriment in the current market. “In the last year when equities are down 15 to 20 per cent fixed interest returns are positive,” says Lance Pupelis, head of cash and fixed income at EQT.

That is despite the low interest rate environment. And the volatility on the share markets has made bonds attractive, pushing up capital values, Pupelis says.

The big risk with bonds in a low interest rate environment is, of course, the prospect of interest rate rises. If rates rise the capital value of a bond will fall because theoretically a new bond of the same capital value would be issued at a higher interest rate. That means the existing bond has to fall in price such that its yield is the same as the new bond with a higher interest rate.

But Pupelis remains sanguine about this risk. “It’s unlikely that there’s going to be a return to high inflation any time soon. So the upside driver on interest rates globally is not obvious.”

A fixed income fund could help insulate investors from rising rates by changing the overall maturity profile of their investments. “In the fixed income universe there is a raft of investments from cash to 15 or 20 years.”

The Australian fixed income universe has an average maturity of around four and a half years. “If we suddenly became concerned about rising interest rates we would shorten that profile to preserve and protect capital while it the move to higher rates was playing out. There are mechanisms we can employ to do that,” Pupelis says.

comments